Global AI Orchestration Market: A Deep-Dive Analysis (2024–2030)

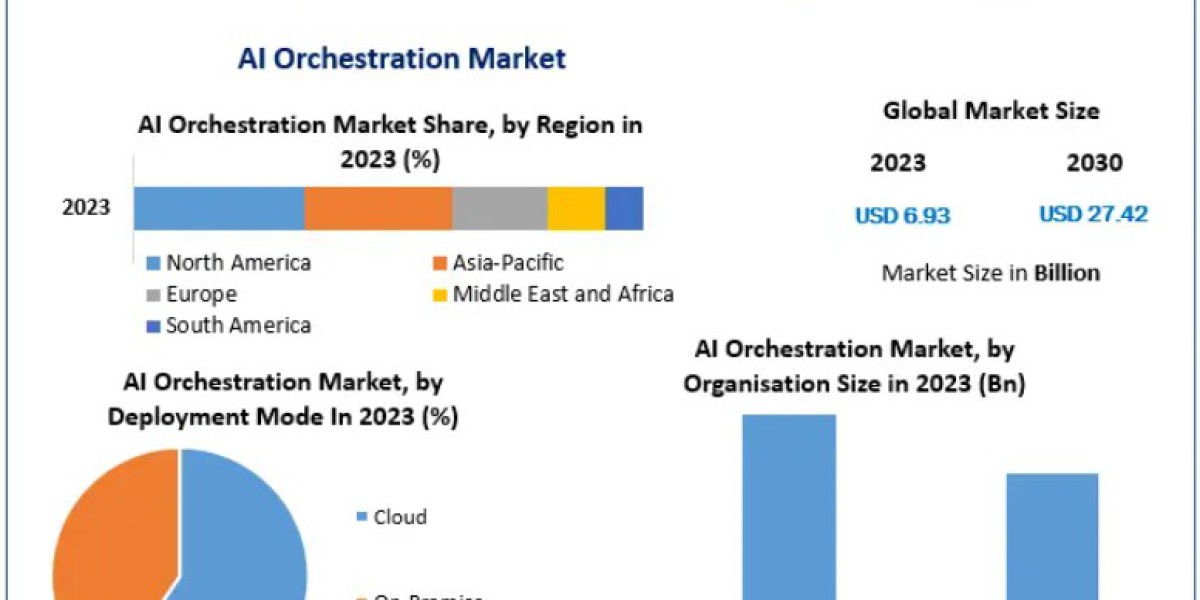

Market Size (2023): USD 6.93 Billion

Forecast (2030): USD 27.42 Billion

CAGR (2024–2030): 21.7%

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/184156/

Introduction

Artificial intelligence is rapidly blending into the operational core of modern enterprises, but its true power is realized only when organizations orchestrate AI workflows efficiently and consistently. This is where AI orchestration solutions step in—serving as the backbone for managing and automating the end-to-end lifecycle of AI and machine learning systems.

From data ingestion and model development to deployment, monitoring, and optimization, AI orchestration platforms eliminate manual inefficiencies, accelerate time-to-value, and enable businesses to transform raw data into actionable intelligence at scale. As industries shift toward automation, intelligent cloud infrastructures, and data-driven ecosystems, the global AI Orchestration Market is experiencing remarkable momentum.

Market Overview

The AI Orchestration Market has expanded from USD 6.93 billion in 2023 to a projected USD 27.42 billion by 2030, driven by the surge in enterprise AI adoption, the proliferation of cloud technologies, and the increasing need to manage complex AI workloads across hybrid and multi-cloud environments.

Organizations are deploying orchestration solutions to unify workflows, automate routine tasks, and ensure consistent governance for all AI-driven initiatives. Industries such as banking, healthcare, manufacturing, e-commerce, and government are among the top adopters.

Market Dynamics

- Drivers

Growing Enterprise Adoption Across Verticals

Enterprises that rely heavily on digital operations—such as retail, BFSI, healthcare, and telecom—are embedding AI deeper into their services, with orchestration becoming essential for efficiency, cost reduction, and process reliability. Banks, for instance, use orchestration to automate compliance checks, detect fraud patterns, and optimize resource deployment.

Rise of Remote Work and Digital Acceleration

The work-from-home era amplified the need for automation across distributed environments. AI orchestration has been instrumental in managing cloud workloads, securing data pipelines, and enabling seamless multi-platform integration.

Collaborative Technology Ecosystems

Strategic partnerships—like IBM’s orchestration initiatives or Cisco and IBM’s integration for 5G network automation—are accelerating innovation and expanding product capabilities.

- Opportunities

Rapid Advancements in Cloud, Big Data & IoT

The expanding digital infrastructure across emerging markets, coupled with cloud-native development, fuels new possibilities for AI lifecycle automation. Organizations pursuing large-scale data analytics and real-time insights prefer orchestration platforms to streamline and manage complex AI pipelines.

AI-Driven Automation of Future Networks

AI combined with Software-Defined Networking (SDN) enables autonomous, self-optimizing cloud and network environments. As 5G matures, AI orchestration will be crucial in managing distributed applications, optimizing service quality, and securing data-intensive workloads.

- Restraints

Data Privacy & Cybersecurity Challenges

With AI systems touching sensitive datasets, concerns around compliance, data exposure, and security vulnerabilities can slow adoption. Breaches in government or enterprise repositories highlight the risks of automated data processing, making robust governance frameworks essential.

Market Segmentation

By Component

- Solutions (Dominant Segment):

Platforms enabling data prep, model training, deployment, and monitoring. Surge in data volume and model complexity boosts demand. - Services:

Includes consulting, integration, and managed services supporting orchestration deployments.

By Deployment Mode

- On-Premise (Leading in 2023):

Preferred by industries handling sensitive data due to stronger control and security. - Cloud (Fastest-Growing):

Low upfront cost, rapid scalability, and easier integration are pushing cloud-based orchestration adoption.

By Application

- Customer Service Orchestration (Largest Segment):

Used for intelligent routing, automated responses, and cross-channel workflow integration. - Infrastructure Orchestration

- Manufacturing Orchestration

- Workflow Orchestration

- Others

By Organization Size

- SMEs (Largest Share in 2023):

AI orchestration empowers SMEs to automate inventory, logistics, and customer workflows without large IT overhead. - Large Enterprises:

Using orchestration to scale AI across departments and modernize legacy infrastructures.

By End Users

- Healthcare (Leading Segment):

AI orchestration enhances patient care journeys, optimizes scheduling, and improves operational efficiency. - IT & Telecom

- Manufacturing

- BFSI

- Retail & Consumer Goods

- Government & Defense

- Energy & Utilities

- Others

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/184156/

Regional Insights

North America – Market Leader

North America continues to dominate due to high cloud adoption, the rise of intelligent virtual assistants, and deep integration of AI in enterprise workflows. The U.S. remains the strongest contributor, supported by tech giants and strong digital infrastructure.

Europe

Strong regulatory frameworks and ongoing digital transformation boost adoption, particularly in manufacturing, government services, and healthcare.

Asia Pacific – Fastest Growing

Countries like China, Japan, India, and South Korea are rapidly modernizing their industries. Government initiatives supporting digital transformation and massive investments in AI R&D create fertile ground for orchestration platforms.

Latin America & Middle East/Africa

Growing cloud adoption and modernization efforts in BFSI, telecom, and energy sectors are gradually increasing market penetration.

Competitive Landscape

Key Players:

- Oracle Corporation

- Fujitsu Limited

- Wipro Limited

- Capgemini Services SAS

- General Electric Company

- BMC Software, Inc.

- TIBCO Software Inc.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

Strategies observed:

- Advancements in AI engines and automation layers

- Cloud integration improvements

- Partnerships for R&D and joint development

- Mergers & acquisitions to strengthen product portfolios

Recent Highlights

- Oracle & NVIDIA Partnership (2022): Bringing full AI-accelerated computing stack to OCI.

- Wipro & Pandorum Technologies (2022): Developing AI models for regenerative medicine.

- Fujitsu & Hexagon Collaboration (2022): Working on digital twin-driven solutions for industrial sustainability and efficiency.

Conclusion

The AI Orchestration Market is entering a high-growth phase where automation, intelligent workflow management, and unified AI operations will become indispensable for businesses worldwide. With advancements in AI, cloud technologies, and big data ecosystems, orchestration platforms will continue shaping the future of digital enterprises.

The market’s evolution from USD 6.93 billion to USD 27.42 billion by 2030 underscores its strategic significance—marking AI orchestration not just as a technological upgrade but as a mission-critical driver for enterprise intelligence, agility, and competitiveness.